The recent crypto market turmoil has been headlined by a series of cascading events, including the collapse of Terra UST and the failure of famed hedge fund, Three Arrows Capital (3AC). Most notable and perhaps most impactful is the rash of distressed centralized crypto lending platforms, which have disproportionately caused harm to retail investors.

These investors have been blindsided by the halting of withdrawals imposed by troubled firms such as BlockFi, Celsius, Voyager, and many more. The headlines paint a story stranger than fiction with rumors of CEOs fleeing the country and the emergence of a new age John Pierpont Morgan to bail out the industry. Blockchain sleuths track the digital trail to uncover hidden wallets and obscured transactions like scenes from a Hollywood movie.

As the dust settles, questions will undoubtedly require answers. How did crypto lenders fail? What happened to customer money? How can investors be protected going forward? Bits of public information, such as the Voyager bankruptcy filing, can help piece together some preliminary answers.

Veneer of competence and security

On the surface, Voyager Digital has many attributes of a qualified business institution. Voyager is a publicly listed company, trading under the ticker VOYG on the Toronto Stock Exchange. The company’s CEO, Stephen Ehrlich, had extensive experience in traditional finance (TradFi), previously serving as CEO of E*TRADE Professional Trading.

Voyager’s website goes on to tout its status as “Publicly traded, licensed and regulated. Honesty and transparency are our top priorities.” In reality, the comprehensive regulatory frameworks applied to TradFi simply do not exist yet for the crypto industry. Even Voyager’s own risk disclosure will tell you that “Cryptocurrencies are not regulated or are lightly regulated in most countries, including the United States.”

What may be the most controversial of Voyager’s marketing tactics is their message on Federal Deposit Insurance Corporation (FDIC) insurance, stating “Your USD is held by our banking partner, Metropolitan Commercial Bank, which is FDIC insured, so the cash you hold with Voyager is protected.” Voyager neglects to complete the sentence, which should read that the cash is protected from the failure of MC Bank, not Voyager itself. As reported by Forbes, the FDIC is now investigating Voyager for potential false advertising and misrepresentation.

Retail investors gut-punched

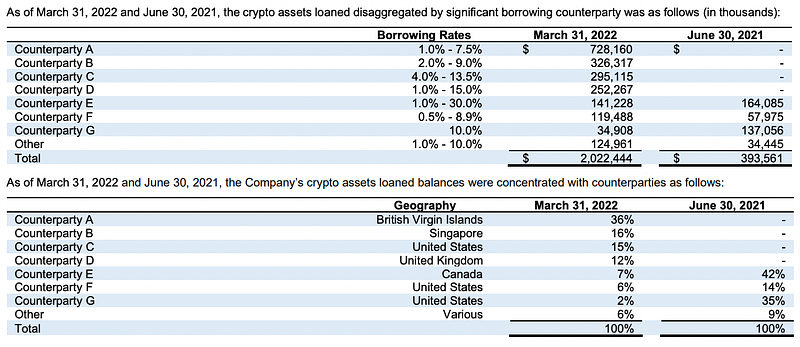

The Voyager bankruptcy filing reveals that Three Arrows Capital defaulted on loans totaling 15,250 BTC and 350 million USDC in June 2022. These loans constituted over 50% of Voyager’s loan book as of its first quarter 2022 public filing. Not only were the loans uncollateralized, they also represented a highly concentrated exposure to a single counterparty.

Source: “Interim financial statements/report — English” May 16, 2022

Note: Using estimated spot prices of BTC in March, we can surmise that 3AC’s loan total roughly $1bn dollars, which approximates the sum of Counterparty A and B, whose registration in BVI and Singapore matches that of 3AC.

The bankruptcy filing also reveals that the vast majority of its 50 largest unsecured claims are represented by customers ranging from $9,771,026.39 down to $955,417.27. Most of these customers are not quite large enough to be institutions and are very likely to be retail investors.

As with the previous collapse of Terra UST, an outpouring of agonizing stories from angry and distraught customers flooded the internet. Journalist Laura Shin detailed the experience of Jess Archer, a Voyager customer who was attracted by the advertised 9% reward for USDC deposits and the perceived safety of stablecoins over more volatile cryptocurrencies. Archer is now one of the many unsecured creditors of Voyager with over $70,000 tied up in bankruptcy court; money she intended as a down payment for a home for herself and two children.

Deposits are not all equal

It is now abundantly clear that a cryptocurrency deposit into a centralized crypto platform is nothing at all like a fiat deposit into an FDIC-insured bank. The nebulous treatment of cryptocurrency deposits under insolvency became a hot topic in May when Coinbase disclosed in its quarterly 10-Q filing, that crypto assets held on behalf of customers could be subject to bankruptcy proceedings and those customers could become unsecured creditors. In truth, Voyager did also make similar statements in its user agreement;

“Customer explicitly understands and acknowledges that the treatment of Customer Cryptocurrency in the event of a Customer, Voyager, or Custodian insolvency proceeding is unsettled, not guaranteed, and may result in a number of outcomes that are impossible to predict, including but not limited to Customer being treated as an unsecured creditor and/or the total loss of all Customer Cryptocurrency.”

Moreover, Voyager telegraphed its risky lending business, such as its unsecured loans to 3AC, in the same user agreement under “Consent to Rehypothecate” in section 5.D;

“Customer grants Voyager the right, subject to applicable law, without further notice to Customer, to hold Cryptocurrency held in Customer’s Account in Voyager’s name or in another name, and to pledge, repledge, hypothecate, rehypothecate, sell, lend, stake, arrange for staking, or otherwise transfer or use any amount of such Cryptocurrency, separately or together with other property, with all attendant rights of ownership, and for any period of time and without retaining a like amount of Cryptocurrency, and to use or invest such Cryptocurrency at Customer’s sole risk.”

Customers deposited cryptocurrency to Voyager and a balance appears in the beautifully constructed mobile app. What perhaps is lost on the customer is that the platform now has broad rights to use those funds, including lending them to hedge funds. Due to the commingled nature of customer crypto assets, it is difficult to even disentangle what portion of a customer’s assets have been hypothecated, lent, or used. In the aftermath of the bankruptcy, Voyager proposes the following, “Customers with crypto in their account(s) will receive in exchange a combination of the crypto in their account(s), proceeds from the 3AC recovery, common shares in the newly reorganized Company, and Voyager tokens,” a far cry from the original balances shown in customer’s mobile apps.

Hard lessons learned

Is it especially heart-wrenching to see risk-conscious retail investors like Jess Archer face uncertainty over their savings when they perhaps believed their crypto deposits were safeguarded as bank deposits would. Bank deposits are not without risks and Circle (USDC stablecoin issuer) noted that “holding any material amount of cash at any bank carries exposure to the counterparty and credit risk of that bank.”

However, banks do operate under mature laws and a robust regulatory framework. Procedures are clearly laid out in the event of a bank failure and there is never a doubt where depositors lie within the priority of payment. According to the FDIC, “No depositor has ever lost a penny of insured deposits since the FDIC was created in 1933.”

The bottom line is, crypto deposits at a crypto lending platform are nothing like traditional bank deposits. The key differentiation is one operates largely without regulation and the other is heavily regulated. Retail customers need a trusted environment that does not put them in peril if they missed the fine print on rehypothecation. Regulatory oversight can help establish a baseline for safe and sound operations and proper governance and management of a centralized crypto platform. Furthermore, regulation will help customers better understand how their funds are stored and protected and what legal claims they have to those funds under normal and exceptional circumstances.

The bar needs to be raised for centralized operators in the crypto industry. Purists will hark back to the adage of “not your keys, not your coins.” To take a more moderate viewpoint, perhaps ownership is not solely conferred by self-custody of private keys but can also be conferred in a more transparent and rigorous manner protected by law and regulation. For the centralized operators, the mantra could be “not your keys, but still your coins, under all plausible and foreseeable scenarios, even under bankruptcy.”

Author: 邢智超, XREX Director of Risk Management

This article was first published on Forkast News “What in crypto hell just happened to all your money?”